|

|||||||||||||

|

|||||||||||||

| Ad Spend Increases More Than Predicted. Good News for Publishers? |

Image sourced from Mediapost

|

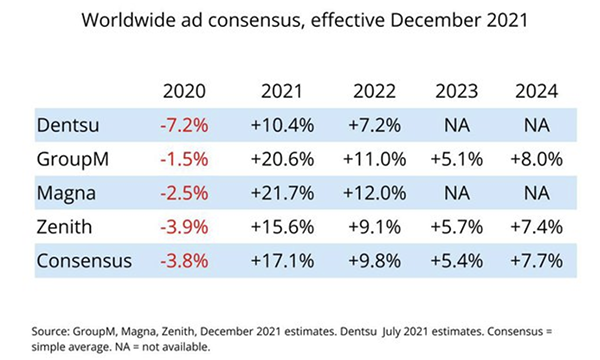

| Consumers hear supply chain issues and walk past empty store shelves and think that the economy's outlook is slow to recover. The ad industry is quite the opposite, posting better than expected gains for 2021 and larger 2022 profit estimates than expected. Profits are imbalanced and most of the dollars goes to the big three: Google (Alphabet), Facebook (Meta) and Amazon. GroupM noted in its forecast that Alphabet, Amazon and Meta take up 80-90% of the global pie. Three companies account for more than the lion’s share … practically the entire lion! Will this trickle down to small businesses, who skyrocketed this industry to unprecedented growth during a global pandemic when they placed more ad dollars into digital than traditional ad mediums. |

| “I think this is possibly the fastest growing year ever in terms of the ad industry, and that is well worth noting,” said GroupM Business Intelligence Global President Brian Wieser. GroupM increased their 2021 U.S. growth estimate by a staggering 6.2 percentage points to 22.7%. The holding company also increased its 2021 growth estimate for worldwide ad spending up 3.3% to 20.6%. Digital is rocking, but TV will take until 2023 to fully recover. “TV ad spending looks set to take until 2023, when GroupM’s estimate calls for it to hit $168.6 billion, to reach and exceed the same levels as in the pre-COVID year 2019 ($167.8 billion), it predicted.” 2023 will be a telling year for publishers when the third-party cookie is slated to disappear forever. Revenue will be impacted significantly and unfortunately, it doesn’t appear that publishers will be recouping their losses in the upcoming months or maybe even years. That’s especially given the way the big three have brought in money hand over fist. Then again, if the federal government and international authorities make good on their claims against big tech, perhaps the tables will turn and we’ll see a much more equitable playing field for both publishers and ad tech vendors. Maybe? “Digital advertising accounted for 64.4 percent of all advertising in 2021, up from 60.5 percent in 2020.” “The need for marketers to directly reach consumers has also led to the success of retailers like Walmart, Target, and Kroger to rapidly grow their own ad sales businesses, allowing brands to use their shopper data to target more customers. This form of advertising grew 47% this year to total $77 billion and is expected to grow to $143 billion by 2024, according to Zenith.” Walmart, Target, and Kroger are not the big three, but they are far from hurting, unlike smaller businesses and pubs that have been reeling from losses over the past 18 months. Typically, the ad industry recovers in line the way the overall economy does. In this instance, it’s been quite the 180, with the ad industry bouncing back bigger, better, and faster than overall recovery. That’s not to say that all’s doom and gloom digitally, but is it enough to make companies whole, following an unprecedented 2020-onward? “Internet-connected TV continues to capture consumer eyeballs and more robust ad tech. Magna Global and Zenith both highlighted e-commerce as another important driver of investment. Zenith described e-commerce as not only the development of shopping platforms, but also brand advertising to promote those offerings, performance media to drive traffic to them and the proliferation of retail media, where marketplaces double as venues for other brands to run ads. Retailer media saw 47% growth in 2021 to reach $77 billion, per Zenith, now making up one-fifth of all expenditures on digital display and paid search.” |

|

| An Embarrassment of Identity Choices | ||

| Do publishers have too much of a good thing with the overabundance of identity solutions to choose from? With more than 80 identity solutions in the market today, analysis paralysis may very well be plaguing publishers to their own detriment. How do you solve a problem like identity selection? Per Lotame’s report “Beyond the Cookie: Identity Solution Testing & Adoption Among Marketers and Publishers,” the choice(s) is simple. Nearly 4 in 5 publishers are open to using multiple identity solutions. Publishers do indeed have an embarrassment of opportunities and options to test which mix of solutions works best for their business. Not surprisingly, data privacy is the number-one driver for publishers to test identity solutions, followed close behind by Google Chrome’s impending third-party cookie death. There’s a lot to lose if publishers don’t take this time to find the right mix of solutions to ensure privacy compliance and preserve monetization. |

||

| A fully cookieless world is just around the corner. The early birds to identity solution testing and adoption are reaping the benefits, and then some. But the industry as a whole seems to have lost some of its urgency to take definitive action via testing and tweaking, opting for more talk of what the future holds. Large publishers are making big bets on first-party data and contextual targeting but those options won’t scale for the longtail. What’s good for the goose, in this case, stinks on ice for the gander. Smaller publishers are getting short shrift in many of these industry-wide conversations that focus on a single solution, but an identity portfolio, including the cookieless Lotame Panorma ID™, offers them not only a fighting chance but a profitable future. To see more of the “Beyond the Cookie” research findings, click here |

||

|

||

| Can Birds of a Different Feather Eventually FLoC Together? |

| Google’s director of product management, David Temkin confirmed one of the many reasons behind the delayed demise of Chrome’s third-party cookies - “FLoC [Google’s Federated Learning of Cohorts] is a proposal – it will evolve. There will be other birds. There are already a lot of birds.” You know TURTLEDOVE and SPARROW and PARRROT and SWAN. But do you recall the most famous bird of them all? The timeline for discontinuing third-party cookies was extended to the end of 2023 to garner additional feedback and allow time for everyone to prepare accordingly. The only problem is the birds are continuing to fly down, with opposing opinions and a large enough stake to hold up any significant movement. While the initial standoff was browser vs. browser (Chrome vs. Everyone - Edge, Safari, Firefox, Vivaldi, etc.), the UK’s Competition and Market Authority’s (CMA) current antitrust investigation into Google’s Privacy Sandbox has raised even more eyebrows around its power imbalance and the potential need for a federal regulator to assess both antitrust and privacy simultaneously. |

| Ever since the dissolution of third-party cookies was announced in January 2020, it has loomed over advertisers, publishers, regulators and even users like a ticking time bomb. What’s worse is the clock is counting down as more time keeps being added, creating an unavoidable paradox that will make any sane stakeholder crazy. The truth is announcing the death of the cookie and actually killing it is proving to be more difficult than expected, even for Google. People don’t like change, especially when it impacts their money, their values, or their convenience. This will significantly impact all of the above and no one is falling in line until all (or at least most) of their demands are met. This includes Google whose parent company, Alphabet attributed 80% of its $183 billion revenue in 2020 to its ad business. It’s no wonder there’s a call for Congress to step in and provide a balance between the promotion of competition and privacy protection. If that happens, it’s best to be prepared for another extension beyond 2023. However, we don’t recommend using this time to sit back and relax. It’s just more time to make sure that when the majority of the adtech industry is on a semi-leveled playing field, your platform is ready to perform without third-party cookies. Whether it’s an evolved version of FLoC or an alternative solution developed through industry collaboration, third-party cookies are going away soon...we just don’t really know when. |

|

||||||||

|

||||||||

|

||||||||

|

||||||||

|

||||||||

|

|

|